Building strong business credit is essential for small business owners, entrepreneurs, and startup founders who want to secure financial growth and stability.

This guide explains how to establish business credit step by step, offering insights into its benefits and practical tips for success.

What Is Business Credit and Why It’s Important?

Source: CRED

Business credit is a measure of your company’s financial reputation. It shows how well your business can handle borrowing money and paying it back on time.

Unlike personal credit, which focuses on your individual finances, business credit is all about the financial health of your company.

Why Is Business Credit Important?

Strong business credit offers several advantages that can help your business grow:

1. Better Loan Opportunities

Lenders are more likely to approve loans for businesses with good credit. You’ll also enjoy benefits like:

- Lower interest rates.

- Access to larger loan amounts.

- Easier approval for financing.

2. Stronger Supplier Relationships

Good business credit makes suppliers more willing to work with you. It can help you:

- Get better payment terms, like paying later for goods or services.

- Build trust and secure reliable partnerships.

3. Protection for Personal Finances

Keeping your personal and business finances separate protects your personal assets. This separation ensures that your personal credit won’t be affected by your business activities and vice versa.

In short, building and maintaining strong business credit is a smart move for any business owner. It opens doors to more opportunities, improves cash flow, and ensures financial stability for your company.

Steps to Establish Business Credit

Source: Smart Business Funding

To understand how to establish business credit, follow these actionable steps:

1. Set Up a Legal Business Structure

The first step in building business credit is to establish your business as a separate legal entity. This means creating a clear distinction between your personal finances and your company’s finances.

How to Do It:

- Choose a legal structure such as an LLC (Limited Liability Company), corporation, or partnership.

- Register your business with the appropriate government authorities in your region.

- Obtain all necessary business licenses and permits.

Why It Matters:

Lenders and suppliers are more likely to trust and work with a business that operates as a formal entity. Additionally, this step protects your personal assets from business liabilities.

2. Obtain a Business Tax ID (EIN)

An Employer Identification Number (EIN) is essential for identifying your business for tax purposes and building credit. Think of it as a Social Security number for your business.

Steps to Get an EIN:

- Visit the IRS website and complete the free online application.

- Provide basic information about your business, such as its name, address, and structure.

- Once approved, you’ll receive your EIN instantly.

Why It’s Important:

An EIN is required to open business bank accounts, file taxes, and apply for loans or credit. It’s the first step toward establishing your business’s financial identity.

3. Open a Business Bank Account

A dedicated business bank account helps separate your business and personal finances, creating a clear financial paper trail. This separation is crucial for managing cash flow and demonstrating financial responsibility to lenders.

Steps to Open an Account:

- Research banks offering business accounts with low fees and benefits tailored to businesses.

- Provide your EIN, business registration documents, and ID.

- Use the account exclusively for business transactions.

Benefits:

- Simplifies bookkeeping and tax preparation.

- Establishes financial credibility with banks and lenders.

- Enables easy tracking of income and expenses.

4. Apply for a Business Credit Card or Trade Lines

To start building your business credit, apply for credit tools designed for businesses. These can include:

- Business Credit Cards: These cards are designed for business expenses and often come with rewards, cashback, or low-interest rates.

- Trade Lines: Work with suppliers who extend credit for purchases, allowing you to “buy now and pay later.”

How to Use Them Effectively:

- Only spend what you can afford to repay.

- Always pay your balances in full and on time.

- Look for credit providers that report to business credit bureaus like Dun & Bradstreet, Experian, or Equifax.

Why It’s Important:

These tools help establish a payment history, which is a key factor in building business credit.

5. Build Relationships With Suppliers and Vendors

Your relationships with suppliers and vendors play a significant role in improving your credit score. Partnering with reliable suppliers who report payment histories to credit bureaus can give your credit a substantial boost.

Tips for Building Strong Relationships:

- Pay invoices early or at least on time.

- Communicate openly with suppliers about payment schedules.

- Use platforms like Hi-Fella to find reputable suppliers who can support your credit-building efforts.

Benefits:

- Improves your payment history, a major factor in credit scoring.

- Strengthens trust and reliability within your industry.

6. Monitor Your Business Credit Regularly

Keeping track of your business credit is essential for understanding your financial standing and identifying areas for improvement.

How to Monitor Your Credit:

- Use services like Dun & Bradstreet, Experian, or Equifax to check your business credit reports.

- Sign up for credit monitoring tools that send alerts for changes or potential issues.

- Regularly review your credit score to track progress.

Why It’s Important:

- Ensures your credit information is accurate.

- Helps you spot and fix errors that could harm your score.

- Allows you to address negative changes before they escalate.

7. Address Credit Issues Quickly

If your credit score is not improving, take action to resolve the issues. Common steps include:

- Paying down high balances on credit cards or trade lines.

- Avoiding maxing out your available credit.

- Building a strategy to pay bills consistently on time.

Consider Professional Help:

Consult with financial experts who can provide tailored advice to improve your credit profile.

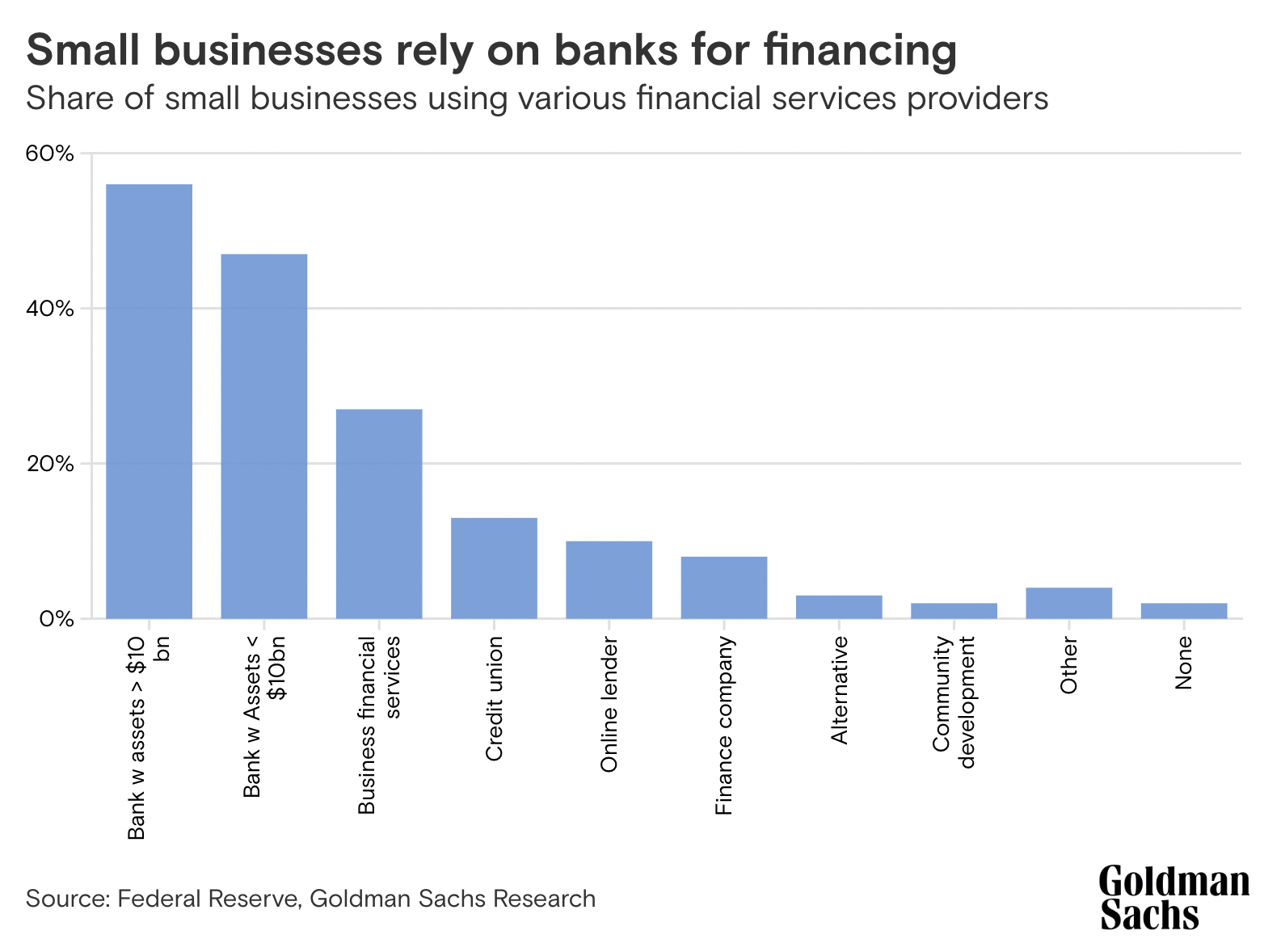

Statistics Highlight Small Business Credit Struggles Amid Banking Stress

According to Goldman Sach, small businesses in the U.S. face growing challenges accessing affordable capital as regional banks tighten credit due to rising interest rates and banking system stress.

While 77% of small business owners expressed confidence in accessing funding last year, the same percentage now voices concern.

With smaller banks providing nearly 70% of small business loans, their struggles disproportionately impact smaller enterprises, further exacerbated by recent bank failures such as Silicon Valley Bank.

Rising interest rates are making it harder for small businesses to manage their existing debt, with 60% of business owners reporting difficulty in servicing their loans.

At the same time, many small business owners feel the economy has worsened, and inflation pressures continue to rise despite government reports suggesting moderation.

However, most are still focused on growth, with 59% looking to hire, though finding qualified candidates remains a challenge. A lack of affordable childcare is another major barrier to getting more workers into the labor market.

Additionally, nearly two-thirds of business owners are worried about the potential impact of a failure to raise the U.S. debt ceiling.

Why Use Hi-Fella to Build Business Credit?

Hi-Fella connects businesses with trustworthy suppliers and partners, enabling you to establish and strengthen your credit profile. By fostering reliable partnerships, Hi-Fella helps:

- Improve payment histories

- Build financial credibility

- Secure better trade terms for long-term success

Understanding how to establish business credit is crucial for long-term financial success. By setting up a legal structure, maintaining separate finances, and building strong relationships with suppliers through platforms like Hi-Fella, you can get better financial opportunities and grow your business confidently!